Andresr | E+ | Getty Pictures

For retirement “tremendous savers,” superior fiscal habits surface to go significantly over and above fattening up their nest eggs, a new research demonstrates.

Most of these personnel — whose 401(k) contributions are at the very least 15% of their pay or 90% or far more of the utmost authorized — also spend their payments on time (87%) and never overdraw their examining account (74%), according to Principal’s 2022 Super Saver Study.

associated investing information

The report, which will come amid raging inflation, increasing curiosity rates and some converse of an financial economic downturn, was based mostly on a latest survey of 1,120 men and women ages 18 to 57 with cash flow ranging from less than $35,000 to far more than $500,000. All of these surveyed fulfill Principal’s definition of a super saver.

Far more from Own Finance:

How to save as food items inflation jumps extra than 11% in a 12 months

Here’s how substantially you can save by secondhand purchasing

Shell out isn’t holding up with inflation. What experts say to do

Whilst the idea of turning out to be a super saver may perhaps seem to be challenging, authorities say that compact variations in practices and lifestyle can go a extended way in assisting workers increase contributions.

“I convey to people that good cash behaviors aren’t much too much from excellent feeding on routines,” said Kathryn Hauer, a certified economical planner with Wilson David Financial investment Advisors in Aiken, South Carolina.

“You continue to be the slimmest when you believe about just about every morsel of food stuff you place in your mouth, and you build the most prosperity by scrutinizing just about every penny you part with,” Hauer said.

Tremendous savers travel old automobiles, steer clear of industry problems

Principal requested people surveyed what “sacrifices” they have created to help save for retirement. For example, 49% push an more mature car or truck, 40% never vacation as significantly as they’d like and 39% say they individual a modest dwelling.

They also have taken methods to shift their funds way of thinking. Several (69%) also do not fret about “maintaining up with the Joneses,” so to speak, and additional than fifty percent really don’t shed sleep around their funds (56%).

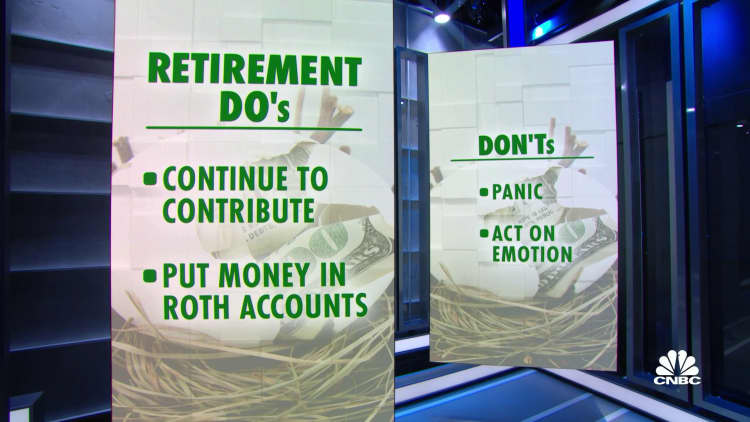

Inventory industry volatility has not frightened off tremendous savers, both: Almost 3-quarters of them look at the latest marketplace ecosystem a purchasing prospect — a person in which they can get shares at a price reduction.

This look at comes in the midst of the important indexes becoming down by double digits this yr. By means of Wednesday’s close, the S&P 500 experienced slid 17.2%, the Dow Jones Industrial Common was off 14.4% and the tech-laden Nasdaq Composite experienced missing 25%.

Small variations in behaviors can enhance financial savings

Although some households may well have tiny to no wiggle area in their budget to conserve more for retirement, other individuals may perhaps just have to have to modify their shelling out to free up additional cash for very long-term savings.

Hauer said that individuals are inclined to spend a lot more funds when they are in “an extreme emotional minute,” which can trigger decisions that or else may perhaps not materialize.

“It could be at a boutique buying for the ideal prom gown for your daughter or at the automobile supplier when you get swept up by interesting added functions on [a car],” Hauer claimed.

If boosting retirement price savings on a common foundation is tough with your recent spending budget, consider stashing absent the occasional additional dollars that will come your way, these as a birthday reward or some of your tax refund.

“Fall surprise income into a retirement account,” Hauer encouraged.

In 2022, workers can stash a highest of $20,500 in their 401(k), with those people age 50 or more mature permitted an additional $6,500 in so-known as capture-up contributions (for a full of $27,000). For individual retirement accounts, the 2022 contribution restrict is $6,000 (with an extra $1,000 permitted as a capture-up volume).